A Guide to Understanding Your Debt Limits and Making Informed Financial Decisions

Debt can be a useful tool for achieving your financial goals, whether it’s buying a house or starting a business. However, taking on too much debt can quickly become overwhelming and lead to serious financial trouble.

That’s why it’s important to determine how much debt you can really handle before taking on any major financial commitments. Understanding your financial limits will help you make more informed decisions and avoid a potential debt trap.

One of the first steps in determining your debt capacity is evaluating your income and expenses. You need to have a clear understanding of how much money you have coming in and how much is going out each month. This will give you an idea of how much room you have in your budget to handle debt payments.

Next, consider your debt-to-income ratio. This is a measure of how much of your income goes towards debt payments each month. Ideally, your debt-to-income ratio should be below 40%. Anything higher than that might be a sign that you’re taking on too much debt that you can’t afford.

Another important factor to consider is your credit score. Lenders use your credit score to assess your creditworthiness and determine the interest rates they offer you. If your credit score is low, it might be a sign that you’re not handling your current debt well and taking on more debt could pose a risk to your financial health.

Lastly, it’s crucial to consider your future financial goals and obligations. If you have plans to start a family or buy a new car in the near future, taking on too much debt now might limit your ability to achieve those goals. It’s important to strike a balance between your current financial needs and your long-term aspirations.

By evaluating your income, expenses, debt-to-income ratio, credit score, and future goals, you’ll be able to determine how much debt you can realistically handle. Remember, it’s always better to be cautious and avoid taking on too much debt than to find yourself drowning in financial stress.

Understanding Your Debt-to-Income Ratio

The debt-to-income ratio is an important financial metric that allows you to assess your ability to manage your debt. It is a comparison between your monthly debt payments and your monthly income, expressed as a percentage.

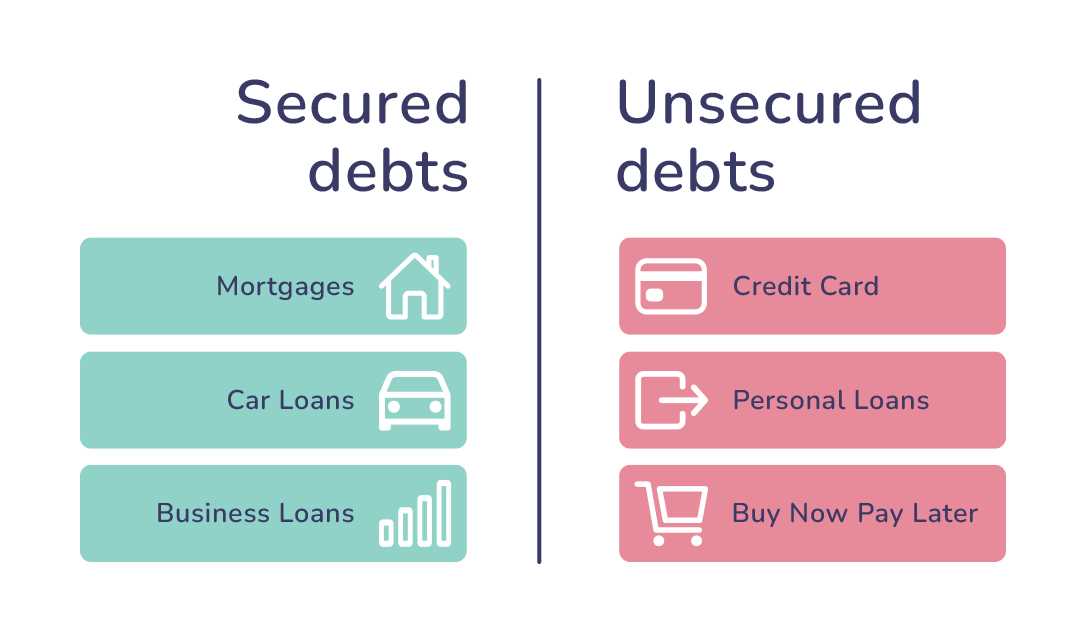

To calculate your debt-to-income ratio, add up all of your monthly debt payments, including housing expenses, car loans, credit card payments, and any other outstanding debts. Then, divide that total by your gross monthly income.

For example, if your total monthly debt payments amount to $2,000 and your gross monthly income is $6,000, your debt-to-income ratio would be 33.33% (2,000 ÷ 6,000 = 0.3333).

A lower debt-to-income ratio is generally considered more favorable, as it indicates that you have more disposable income available to cover your debt obligations. Lenders often use this ratio to assess your creditworthiness and determine your eligibility for loans or other lines of credit.

It’s important to understand that your debt-to-income ratio is just one factor that lenders consider when evaluating your financial health. Other factors, such as your credit score, employment history, and total assets, may also be taken into account.

If your debt-to-income ratio is high, you may want to consider reducing your debt or increasing your income to improve your financial situation. This could involve paying off outstanding debts, finding ways to increase your income, or seeking professional financial advice.

By understanding and monitoring your debt-to-income ratio, you can gain valuable insight into your overall financial stability and make informed decisions about managing your debts.

Calculating Your Monthly Cash Flow

To determine how much debt you can handle, it’s crucial to calculate your monthly cash flow. This will give you a clear picture of how much money you have coming in and going out each month.

Start by adding up all of your sources of income, including your salary, any freelance work, rental income, or investment returns. Be sure to include the after-tax amounts, as it’s the net income that you can use to pay off debt.

Next, make a list of all your monthly expenses. This should include necessities such as rent or mortgage payments, utilities, groceries, transportation costs, and healthcare expenses. Don’t forget about any debt payments you’re already making, such as student loans or credit card payments.

Once you have your income and expenses calculated, subtract your total expenses from your total income to determine your monthly cash flow. This is the amount of money you have left over each month to put towards debt payments or savings.

If your monthly cash flow is positive, that means you have money left over after covering your expenses. This is a good sign and indicates that you have some flexibility when it comes to taking on additional debt.

On the other hand, if your monthly cash flow is negative, you’re spending more than you’re earning. This is a warning sign and means you need to take a closer look at your expenses and find ways to cut back. It’s not wise to take on more debt in this situation, as it will only increase your financial burden.

Remember, calculating your monthly cash flow is an essential step in determining how much debt you can handle. It provides a realistic view of your financial situation and helps you make informed decisions about your debt management strategies.

Understanding your own financial health and recognizing your limits is crucial to avoid taking on more debt than you can handle.

Evaluating Your Fixed Expenses

Fixed expenses are those regular, recurring payments that you have to make each month, regardless of your financial situation. Evaluating your fixed expenses is an important step in determining how much debt you can really handle.

List Your Fixed Expenses

The first step in evaluating your fixed expenses is to make a comprehensive list of all your fixed expenses. This includes things like rent or mortgage payments, car payments, insurance premiums, and utility bills. Be sure to include all necessary expenses, even if they are small.

It can be helpful to look back at your bank statements and bills from the past few months to ensure that you haven’t missed anything. Remember to also include any annual or quarterly expenses that you need to budget for.

Calculate Your Monthly Fixed Expenses

Once you have your list of fixed expenses, it’s time to calculate how much you are spending on these expenses each month. Add up the amounts for each expense to get your total monthly fixed expenses.

Be sure to account for any variable expenses that are typically consistent, such as groceries or transportation costs. These can also be factored into your fixed expense calculations by averaging out your monthly spending over a few months.

Having a clear understanding of your fixed expenses will help you determine how much money you have available to allocate towards paying off debt or taking on new financial obligations.

Assessing Your Variable Expenses

When determining how much debt you can handle, it’s important to take into account your variable expenses. Variable expenses are costs that can fluctuate from month to month and are not fixed. These expenses can include things like groceries, entertainment, clothing, and dining out. It’s essential to assess these expenses to get a comprehensive understanding of your financial situation.

To assess your variable expenses, start by keeping track of your spending. Create a budget and document all your variable expenses for a few months. This will give you a better idea of how much you typically spend and where your money is going.

Once you have a record of your spending, analyze your variable expenses and look for areas where you can make cuts or adjustments. Consider if there are any non-essential items or activities that you can reduce or eliminate. For example, dining out less frequently or finding cheaper entertainment options.

Additionally, think about any areas where you might be overspending. Are there any subscriptions or memberships that you don’t use or could downgrade? Are you buying things impulsively without considering if they are necessary?

After analyzing your variable expenses, you’ll have a clearer understanding of how much money you can allocate towards paying off debt. By making adjustments and being mindful of your spending habits, you can free up more funds to put towards your debt payments and gain better control over your financial situation.

Remember, assessing your variable expenses is an ongoing process. As your financial situation changes, so might your expenses. Regularly reviewing and adjusting your budget will ensure that you stay on track towards your debt-free goals.

Analyzing Your Credit Score

Your credit score is a numerical representation of your creditworthiness and is used by lenders to determine your ability to handle debt. It is important to understand how your credit score is calculated and what factors contribute to it.

Factors Affecting Your Credit Score

There are several key factors that influence your credit score:

- Payment History: Your payment history is the most significant factor affecting your credit score. Paying your bills on time and in full demonstrates your financial responsibility and can positively impact your credit score.

- Credit Utilization: Credit utilization is the ratio of your credit card balances to your credit limits. Using a high percentage of your available credit can negatively affect your credit score.

- Length of Credit History: The length of your credit history is an important factor in determining your creditworthiness. Generally, a longer credit history with responsible credit management is viewed favorably by lenders.

- New Credit: Opening new credit accounts can impact your credit score. Multiple credit inquiries and a high number of recently opened accounts may suggest a higher risk of default.

- Credit Mix: Having a diverse mix of credit types, such as credit cards, mortgages, and installment loans, can demonstrate your ability to manage different types of debt.

Checking Your Credit Score

It is advisable to regularly check your credit score to stay aware of your financial standing. You can obtain a free copy of your credit report once a year from each of the three major credit bureaus: Experian, Equifax, and TransUnion. You can also use online services, such as Portfolio debank, to access your credit score and monitor any changes.

Interpreting Your Credit Score

Your credit score falls within a range that indicates your creditworthiness:

| Credit Score Range | Creditworthiness |

|---|---|

| 300-579 | Poor |

| 580-669 | Fair |

| 670-739 | Good |

| 740-799 | Very Good |

| 800-850 | Exceptional |

A higher credit score indicates a lower risk for lenders, making it easier for you to obtain favorable terms for loans and credit. If your credit score falls below the desired range, there are steps you can take to improve it, such as making timely payments, reducing credit card balances, and avoiding new credit inquiries.

In conclusion, understanding and analyzing your credit score can provide valuable insights into your financial health. Regularly monitoring your credit score and taking steps to improve it can help you effectively manage your debt and achieve your financial goals.

Considering the Impact of Interest Rates

When it comes to taking on debt, one of the most important factors to consider is the impact of interest rates. Interest rates play a crucial role in determining the cost of borrowing money and can have a significant impact on your overall financial situation.

The Effect on Monthly Payments

Interest rates directly affect the amount of money you have to pay each month towards your debt. Higher interest rates mean higher monthly payments, while lower interest rates result in lower monthly payments. It’s important to calculate and consider these monthly payments before taking on any new debt to ensure that you can comfortably afford them.

The Total Cost of Borrowing

Interest rates also determine the total cost of borrowing over the life of your debt. Higher interest rates mean paying more in interest charges over time, which can significantly increase the total cost of the loan. Lower interest rates, on the other hand, result in lower total costs. It’s crucial to carefully evaluate the long-term impact of interest rates on your debt and decide if it’s worth taking on higher costs or if you need to explore alternatives.

In addition to considering the impact of interest rates, it’s also important to factor in other costs associated with borrowing, such as origination fees, late payment fees, and prepayment penalties. These factors can further increase the overall cost of debt and should be taken into account when determining how much debt you can handle.

In conclusion, interest rates can have a significant impact on your ability to handle debt. It’s important to carefully consider the effect of interest rates on monthly payments and the total cost of borrowing before taking on new debt. By doing so, you can make informed financial decisions and avoid taking on more debt than you can comfortably handle.

Assessing Your Financial Goals

Before determining how much debt you can handle, it’s important to assess your financial goals. Understanding your priorities and what you hope to achieve financially will help guide your decision-making process.

1. Short-term Goals

Short-term goals typically cover a period of one year or less. These goals may include things like saving for a vacation, purchasing a new car, or building an emergency fund. Take a moment to identify your short-term goals and consider how much debt you are comfortable taking on to achieve them. Remember to consider your current income and expenses.

2. Long-term Goals

Long-term goals cover a period of multiple years and often involve larger financial milestones. Examples of long-term goals include buying a home, saving for retirement, or funding your child’s education. Evaluate the importance of these goals and how they align with your overall financial plan. Consider factors such as your age, income potential, and risk tolerance when determining how much debt you can handle while still achieving these goals.

By assessing your financial goals, you can align your debt management strategy with your overall objectives. This will ensure that you make informed decisions about how much debt you can handle and minimize the risk of overextending yourself financially.

Estimating Your Future Income

When it comes to determining how much debt you can handle, one crucial factor to consider is your future income. Estimating your future income can help you understand your financial capacity and determine how much debt you can comfortably take on.

1. Assess Your Current Income

To estimate your future income, it’s important to start by assessing your current income. Take into account your salary, bonuses, side hustles, and any other sources of income you currently have. Be sure to consider any potential changes to your income in the near future, such as raises or promotions.

Example: If you earn an annual salary of $50,000 and anticipate a 10% raise next year, your estimated future income would be $55,000.

2. Consider Future Career Changes

In addition to assessing your current income, think about any potential career changes in the future that could affect your income. Will you be transitioning to a higher-paying job or industry? Are there any certifications or additional education you plan to pursue that could lead to higher income opportunities?

Example: If you are planning to switch careers and enter a higher-paying industry, you could estimate a higher future income based on the average salary range for your desired position.

Note: It’s important to research and gather accurate data when estimating your future income based on career changes.

By considering your current income and potential future changes, you can estimate your future income and determine how much debt you can truly handle. This information will help you make informed financial decisions and avoid taking on too much debt beyond your means.

Analyzing Your Current Savings

When determining how much debt you can handle, it’s important to take a close look at your current savings. This analysis will help you understand how much money you have available to pay off your debts and whether or not you have enough to cover your expenses.

1. Calculate Your Total Savings:

The first step is to calculate the total amount of money you have saved up. This includes any money in your checking accounts, savings accounts, certificates of deposit (CDs), or any other type of savings vehicle. Add up all of your savings to get your total savings amount.

2. Consider Your Emergency Fund:

Next, consider your emergency fund. This is money set aside specifically for unexpected expenses, such as medical bills or car repairs. It’s important to have an emergency fund in place before taking on any additional debt. Subtract your emergency fund amount from your total savings to get a more accurate picture of your available funds.

3. Assess Your Expenses:

Take a look at your monthly expenses and determine how much money you need to cover these costs. This should include your rent/mortgage, utilities, groceries, transportation, and any other necessary expenses. Subtract your monthly expenses from your remaining savings to see how much is left over.

4. Determine Debt Repayment Ability:

Now that you have a better understanding of your available funds, it’s time to assess how much debt you can handle. Consider your current monthly debt payments, such as credit card bills, student loans, or personal loans. Compare these payments to the amount of money you have left over from your savings after subtracting your monthly expenses. This will give you an idea of how much additional debt you can manage.

Remember, it’s important to have a cushion of savings and not commit all of your funds to debt repayment. By carefully analyzing your current savings, you can determine what is a feasible amount of debt for you to take on.

Considering Emergency Funds

When it comes to managing debt, it’s important to think about the unexpected. Unexpected expenses can arise at any time, and having an emergency fund in place can help you handle these situations without adding to your debt burden. Here are a few key points to consider when it comes to emergency funds:

1. Building an Emergency Fund

Building an emergency fund should be a priority when managing your debt. Aim to save at least three to six months’ worth of expenses. This can provide a financial buffer in case of job loss, illness, or other unexpected events. Start by setting aside a small amount each month and gradually increase your savings over time.

2. Separate Account

To keep your emergency fund separate and easily accessible, consider opening a separate bank account specifically for this purpose. This can help you resist the temptation to dip into the funds for non-emergency expenses. It’s also a good idea to keep your emergency fund in a liquid and low-risk investment option, such as a high-yield savings account.

3. Regular Contributions

Consistently contributing to your emergency fund is crucial to its effectiveness. Treat it like any other bill or expense and make regular contributions. You can automate these contributions by setting up automatic transfers from your main bank account to your emergency fund account. This way, you won’t forget to save and it becomes a habit.

4. Only for Emergencies

Remember that your emergency fund should only be used for true emergencies. It’s not meant to cover everyday expenses or non-essential purchases. Having a clear definition of what constitutes an emergency will help you avoid depleting your fund unnecessarily.

By considering these points and building a solid emergency fund, you’ll have peace of mind knowing that you’re prepared for unexpected financial challenges without spiraling into further debt.

Evaluating Your Job Security

When considering your ability to handle debt, it is vital to evaluate your job security. The stability of your employment can have a significant impact on your financial well-being. Here are some factors to consider when evaluating your job security:

- Industry Outlook: Research the current and projected future growth of the industry in which you work. If your industry is experiencing decline or instability, it may indicate potential job losses or lack of opportunities for advancement.

- Company Performance: Review the financial health and performance of your employer. If the company is struggling financially or undergoing significant changes, such as layoffs or restructuring, it could signal potential job insecurity.

- Job Competitiveness: Assess your skills and qualifications in relation to others in your field. If you possess specialized knowledge or qualifications that make you highly marketable, you may have more job security compared to others with less desirable skills.

- Employment Contract or Agreement: Review the terms of your employment contract or any agreements you have with your employer. Pay attention to clauses related to job security, such as notice periods or conditions for termination.

- Market Demand for Your Skills: Consider how in-demand your skills are in the job market. If there is high demand for professionals with your expertise, you may have more job security and bargaining power.

- Networking and Professional Relationships: Assess the strength of your professional network and relationships within your industry. A robust network can provide opportunities for job leads or recommendations, enhancing your job security.

By thoroughly evaluating your job security, you can make more informed decisions about the amount of debt you can handle. It is crucial to have a solid understanding of your employment situation to avoid taking on excessive debt that could become unmanageable in the event of a job loss or significant change in financial circumstances.

Assessing Your Current Level of Debt

Before determining how much debt you can handle, it is important to assess your current level of debt. Understanding your current financial situation will give you a clearer picture of where you stand and what steps you need to take to manage your debt effectively.

1. Gather your documents

Start by gathering all your financial documents, including bank statements, credit card statements, and loan agreements. This will give you a comprehensive look at all your outstanding debts and their current balances.

2. Calculate your total debt

Next, calculate your total debt by adding up all your outstanding balances. This includes credit card debt, student loans, mortgage or rent payments, car loans, and any other outstanding debts.

3. Determine your debt-to-income ratio

Your debt-to-income ratio is an essential indicator of your ability to manage debt responsibly. To calculate this ratio, divide your total monthly debt payments by your gross monthly income. Multiply the result by 100 to get a percentage.

For example, if your total monthly debt payments amount to $1,500 and your gross monthly income is $5,000, your debt-to-income ratio would be 30% ($1,500 / $5,000 * 100).

A higher debt-to-income ratio indicates a higher level of debt compared to your income, which may suggest that you are already carrying too much debt.

4. Analyze your monthly cash flow

Assessing your monthly cash flow is crucial in determining how much debt you can handle. Calculate your income and subtract all your fixed monthly expenses, such as rent or mortgage payments, utilities, and insurance. The remaining amount is your disposable income.

This disposable income can be used to pay off debt, cover unexpected expenses, and save for the future. If your disposable income is minimal or negative, it may be an indication that you need to reduce your debt load.

5. Consider your financial goals and priorities

Take into account your financial goals and priorities when assessing your current level of debt. If you have long-term goals, such as homeownership or retirement savings, you may need to adjust your debt load accordingly.

It’s important to find a balance between managing your current debts and working towards your long-term financial objectives.

By assessing your current level of debt, you can gain a better understanding of your financial situation and make informed decisions about how much debt you can handle. This will help you take control of your finances and pave the way for a more secure financial future.

Considering Life Events

When determining how much debt you can handle, it’s important to consider potential life events that might impact your financial situation. These events can include:

- Job loss: Losing your job can greatly impact your ability to repay debts. It’s important to have a plan in place for how you would handle debt payments if you were to lose your source of income.

- Medical emergencies: Unexpected medical expenses can quickly add up and strain your finances. It’s crucial to have a financial cushion or insurance coverage to handle such emergencies and avoid taking on excessive debt.

- Starting a family: The added expenses of starting a family can have a significant impact on your budget. Consider how these additional costs will affect your ability to manage debt and make necessary adjustments to your financial plan.

- Major home repairs: If you own a home, unexpected repairs or maintenance can be costly. You should have funds set aside to cover these expenses without relying on credit cards or loans.

- Education expenses: If you or your dependents are pursuing higher education, it’s important to factor in the costs and potential debt associated with tuition, books, and other related expenses.

By considering these life events and their potential financial implications, you can better determine how much debt you can handle and make informed decisions to protect your financial stability.

Evaluating Your Financial Discipline

One of the key factors in determining how much debt you can handle is evaluating your financial discipline. This involves taking a hard look at your spending habits, saving practices, and overall money management skills.

Creating a Budget

The first step in evaluating your financial discipline is creating a budget. A budget allows you to track your income and expenses, and helps you understand where your money is going. Take the time to sit down and analyze your spending patterns. Are there areas where you could cut back or make adjustments? A budget can help you identify areas where you may need to exercise more discipline when it comes to managing your finances.

Saving and Emergency Funds

Another aspect of financial discipline is the ability to save money and have emergency funds in place. Saving is an essential part of managing debt because it provides a safety net in case of unexpected expenses or income fluctuations. Evaluate your current savings habits and determine if you are setting aside enough money each month. If not, consider adjusting your budget to prioritize saving. Having a solid emergency fund can help prevent you from relying on credit cards or loans when unexpected expenses arise.

| Factors to Consider: | Questions to Ask: | Your Score: |

|---|---|---|

| Spending Habits | Are you living within your means? Do you often make impulse purchases? | |

| Saving Practices | Are you saving consistently? Do you have a designated savings account? | |

| Budgeting Skills | Do you stick to your budget? Do you regularly review and adjust your budget as needed? | |

| Debt Repayment History | Have you successfully managed debt in the past? Do you have a history of late payments or defaults? |

Evaluating your financial discipline is crucial in determining how much debt you can handle. By being honest with yourself and identifying areas for improvement, you can develop better money management habits and make more informed decisions about taking on debt.

Assessing Your Willingness to Make Sacrifices

When it comes to managing debt, one of the most important factors to consider is your willingness to make sacrifices. Taking on debt often requires making lifestyle adjustments and cutting back on expenses. It’s essential to assess your readiness to make these sacrifices before taking on additional debt.

There are several questions you can ask yourself to determine your willingness to make sacrifices:

- Are you willing to cut back on discretionary spending? Discretionary spending refers to non-essential expenses like dining out, entertainment, and shopping. If you’re serious about managing debt, you may need to curb these expenses and prioritize your financial goals.

- Are you willing to delay big-ticket purchases? Sometimes, sacrificing means delaying gratification. Instead of splurging on a new car or the latest gadget, you may need to hold off on these big-ticket items until you have your debt under control.

- Are you willing to downsize your living arrangements? Housing costs often account for a significant portion of an individual’s budget. If you’re struggling with debt, downsizing your living arrangements to a more affordable option might be necessary.

- Are you willing to increase your income? Supplementing your current income through side hustles or part-time jobs can provide additional financial resources to tackle your debt. However, this may require sacrificing leisure time and putting in extra effort.

- Are you willing to negotiate lower interest rates or payment terms? Taking control of your debt also involves reaching out to creditors to explore options for lower interest rates or more manageable payment terms. This process may require time and effort but can ultimately save you money.

Assessing your willingness to make sacrifices is crucial for effectively managing debt. By honestly evaluating your willingness to adjust your lifestyle and make necessary changes, you will be better equipped to handle your debt and achieve financial independence.

Understanding the Psychological Impact of Debt

Apart from the obvious financial implications, having significant debt can also take a toll on an individual’s mental and emotional well-being. The psychological impact of debt is often underestimated, but it can be just as damaging as the financial consequences.

One of the primary psychological effects of debt is stress. Constantly worrying about how to make ends meet, dealing with collection calls, and managing multiple payments can lead to chronic stress, anxiety, and even depression. The burden of debt can consume a person’s thoughts and affect their ability to enjoy life.

Additionally, debt can also impact an individual’s self-esteem. The weight of financial obligations can make people feel inadequate, hopeless, and trapped. They may perceive themselves as failures or believe that they are not capable of regaining control of their financial situation. This negative perception can further contribute to feelings of worthlessness and low self-worth.

Furthermore, the psychological impact of debt can strain relationships. Financial difficulties can lead to arguments, resentment, and a breakdown in communication between partners, family members, and friends. The constant financial pressure can create a tense and hostile environment, putting a strain on even the most resilient relationships.

It is essential to acknowledge and address the psychological effects of debt in order to effectively manage and overcome them. Seeking support from friends, family, or professional counselors can provide valuable emotional assistance. Developing a realistic plan to tackle debt, practicing self-care, and setting achievable goals can also empower individuals to regain control of their financial and psychological well-being.

Remember: Debt is not just a financial burden; it has lasting psychological repercussions. It is crucial to address and manage both the financial and emotional aspects of debt to achieve long-term stability and peace of mind.

FAQ:,

What is debanking?

Debanking is a process of determining how much debt one can handle in order to avoid getting into financial trouble. It involves evaluating one’s income, expenses, and financial goals to come up with a realistic amount of debt that can be comfortably managed.

How can I determine how much debt I can handle?

To determine how much debt you can handle, you need to assess your income, expenses, and financial goals. Start by calculating your monthly income after taxes and subtract your monthly expenses, including necessities such as rent and groceries. Consider any other financial obligations and goals you have, such as saving for retirement or paying for education. This will give you an idea of how much money you have available to put towards debt repayment each month. From there, you can determine how much debt you can comfortably afford by considering factors such as interest rates, repayment terms, and your overall financial stability.

What are some signs that I may be taking on too much debt?

There are several signs that you may be taking on too much debt. These include struggling to make minimum payments on your debts, using credit cards to cover essential expenses, constantly juggling bills and moving balances between multiple credit cards, and feeling overwhelmed by your financial obligations. These signs indicate that your debt load may be too high for your income and financial situation, and it may be time to reassess and make changes to avoid getting into further financial trouble.

Is it ever a good idea to take on debt?

While taking on debt is sometimes necessary, it is important to do so responsibly. It can be a good idea to take on debt for investments that have the potential to generate a positive return, such as a mortgage for a home or a loan for education that will lead to a higher-paying job. However, taking on debt for unnecessary expenses or when you already have a high level of debt can lead to financial problems. It is important to carefully evaluate the potential benefits and risks before taking on any debt.

What can I do if I realize I have too much debt?

If you realize that you have too much debt, there are several steps you can take. First, create a budget to gain a clear understanding of your income, expenses, and debt obligations. Cut back on non-essential expenses and consider finding ways to increase your income. Next, prioritize your debt repayments by focusing on high-interest debts first, while still making minimum payments on all debts. Consider seeking professional help from a financial advisor or a credit counseling agency to help you develop a debt repayment plan and negotiate with creditors. Finally, stay committed to your debt repayment plan and avoid taking on new debt until you have resolved your current financial situation.